China still dominates graphite anode supply, but EV battery makers are rapidly seeking alternatives. New projects across Africa, North America, and Europe are scaling mining, processing, and anode production to reduce dependency. Companies like Syrah Resources, Novonix, POSCO Future M, Talga Group, and Nouveau Monde Graphite are leading this shift. Tools like SourceReady, an AI supplier search engine, help sourcing teams identify verified non-China graphite suppliers and diversify battery supply chains more efficiently.

There’s a better way to source ❤️

Watch the video to see how SourceReady helps brands move from product ideas to trusted supplier relationships faster

Why are graphite anodes suddenly a strategic sourcing problem?

Graphite is the largest material component in a lithium-ion battery by weight. Every EV battery requires roughly 50–100 kg of graphite, mostly used in the anode (the battery’s negative electrode).

The catch: the supply chain is extraordinarily concentrated.

~70–80% of natural graphite mining occurs in China.

~90%+ of anode-grade processing capacity sits there as well.

In other words, even graphite mined elsewhere often travels to China for purification, shaping, and coating before entering EV batteries.

Recent policy shifts accelerated the risk:

Chinese export controls on graphite technologies

Western tariffs and “foreign entity of concern” (FEOC) rules

EV tax credits tied to non-China supply chains

As a result, automakers and battery manufacturers are scrambling to build ex-China supply chains.

For sourcing teams, the question is no longer if diversification happens. It’s who can realistically scale before 2030.

Which Non-China Graphite Anode Producers Are Scaling?

Many graphite projects exist on paper. Few are building industrial-scale anode production.

The following companies represent the most credible non-China suppliers currently scaling capacity.

1. Syrah Resources — Natural Graphite to U.S. Anode Production

Headquarters: Australia

Key Assets: Mozambique + United States

Focus: Natural graphite → Active Anode Material (AAM)

Syrah Resources is building what may become the first large-scale natural graphite anode supply chain outside China.

Core assets

Balama Mine (Mozambique): One of the largest natural graphite deposits in the world.

Vidalia AAM Facility (Louisiana, USA): Processes natural graphite into battery-grade active anode material.

Expansion highlights

The Vidalia plant is undergoing a major expansion, adding roughly 180,000 square feet of processing space.

The project is backed by U.S. Department of Energy funding, including loans and tax incentives.

The company has signed supply agreements with EV manufacturers, including Tesla (though contract terms have fluctuated).

Why it matters

Syrah’s model solves a key supply-chain problem:

Mine graphite outside China → process it in North America → supply Western gigafactories.

For buyers seeking IRA-compliant materials, Syrah is one of the most strategically important suppliers in the market.

2. Novonix — Scaling Synthetic Graphite in the United States

Novonix is positioning itself as a major North American producer of synthetic graphite anodes.

Synthetic graphite is often preferred for:

longer cycle life

faster charging

higher consistency

Expansion highlights

The company is expanding production in Chattanooga, Tennessee.

Target capacity exceeds 50,000 tonnes of synthetic graphite per year by 2028.

Government and partner support

$100 million U.S. Department of Energy grant

Proposed $754.8 million DOE loan

Supply agreements with Panasonic and Stellantis

The total investment could exceed $1 billion, creating over 500 jobs.

3. POSCO Future M — Industrial-Scale Battery Materials Supplier

Headquarters: South Korea

Focus: Graphite anodes and other battery materials

POSCO Future M is part of the POSCO industrial group, one of the largest materials producers in Asia.

Unlike many startups in the graphite sector, POSCO already operates large-scale battery material manufacturing.

Expansion highlights

The company is rapidly expanding EV battery material production globally.

Target: 1 million tons of cathode material capacity by 2030.

Key graphite-related projects include:

Pohang, South Korea: Expanding synthetic graphite production to 18,000+ tons by 2025.

Vietnam (Thai Nguyen Province): Building a $270 million artificial graphite anode plant, with construction starting in 2026 and mass production targeted for 2028.

North America: Expanding battery material capacity through its Ultium CAM joint venture with GM.

Strategic direction

POSCO is also investing in next-generation materials such as:

solid-state battery components

silicon anodes

lithium metal technologies

Why it matters

POSCO Future M combines:

industrial manufacturing experience

deep integration with battery makers

global production footprint

For buyers seeking stable supply at scale, POSCO represents one of the most mature non-China suppliers in the anode market.

4. Nouveau Monde Graphite — Building a Fully Integrated North American Supply Chain

Nouveau Monde Graphite (NMG) is developing one of the most ambitious mine-to-anode graphite supply chains in North America.

The company’s strategy is to integrate mining, processing, and anode production within Québec’s battery materials ecosystem.

Core projects

Matawinie Mine (Québec) NMG’s primary graphite mining operation located in Saint-Michel-des-Saints. The project is designed as an all-electric, low-carbon mine.

Uatnan Project (Phase 3 expansion) Following the acquisition of the Lac Guéret deposit, NMG plans to scale production to as much as 500,000 tonnes of graphite concentrate per year, potentially making it one of the largest graphite projects globally.

Bécancour Battery Material Plant A large-scale processing facility converting graphite concentrate into active anode material (AAM) for lithium-ion batteries.

Strategic partnerships

NMG has secured binding agreements with battery supply chain partners, including:

Panasonic Energy

Traxys

The project also benefits from Canadian government support and financing.

Why it matters

Nouveau Monde is positioning itself as a local North American supplier of low-carbon battery materials.

For automakers and battery manufacturers seeking regional supply chains and ESG compliance, NMG could become a major supplier once full production ramps up later this decade.

5. NextSource Materials — Scaling Graphite Mining in Madagascar

Headquarters: Canada

Primary asset: Madagascar

Focus: Natural graphite mining and downstream anode materials

NextSource Materials operates the Molo Graphite Mine, one of the largest known graphite deposits outside China.

The company is pursuing a phased expansion strategy to significantly increase production capacity.

Expansion highlights

Phase 1 production: The mine began operations in 2023, with initial output of approximately 17,000 tonnes per year.

Phase 2 expansion: The company plans to scale production to roughly 150,000 tonnes per year of graphite concentrate, nearly nine times the initial capacity.

Project financing

To support expansion, NextSource secured a US$91 million debt facility from the International Finance Corporation (IFC).

Downstream development

Beyond mining, the company is developing a Battery Anode Facility (BAF) to convert graphite concentrate into active anode material for EV batteries.

Why it matters

Madagascar is emerging as a critical source of natural graphite outside China.

If expansion proceeds as planned, NextSource could become a major upstream supplier feeding Western battery supply chains.

6. Talga Group — Building a European Graphite-to-Anode Supply Chain

Talga Group is developing a vertically integrated graphite supply chain in Europe, targeting regional EV battery manufacturers.

Production plans

The company is scaling engineering and construction efforts to support a 5,000-tonne-per-year anode production facility in Sweden.

The project draws on Talga’s high-grade graphite deposits in northern Sweden, which contain some of the largest graphite resources in Europe.

Financing and support

Talga recently secured:

$14.5 million capital raise

$13.35 million Swedish government grant

These funds support engineering work and production ramp-up.

Strategic initiatives

Recycling integration: Talga signed an MoU with Altilium to secure up to 16,000 metric tonnes of recycled graphite starting in 2026.

International expansion: The company is evaluating opportunities in the United States, Japan, and the Middle East.

Why it matters

Europe is rapidly building domestic EV battery supply chains.

Talga’s strategy aligns with EU industrial policy by combining:

European mining

local anode production

low-carbon processing

For European automakers, this creates a potential regional alternative to Chinese graphite supply.

Which Regions Are Becoming the New Graphite Supply Hubs?

China will remain a major graphite supplier, but the supply chain is shifting toward a more diversified global structure. Governments and battery makers are investing to build graphite mining and anode production outside China.

Below are the key non-China graphite supply hubs emerging today.

1. Africa — The Fastest-Growing Source of Natural Graphite

Africa is becoming one of the most important regions for new natural graphite mining projects. The continent hosts several large, high-grade deposits capable of supplying EV battery demand for decades.

Countries such as Mozambique and Madagascar already host major projects that supply graphite concentrate to global battery supply chains.

Nouveau Monde Graphite — Integrated supply chain in Québec

North America is emerging as a hub for active anode material production and synthetic graphite manufacturing.

3. Northern Europe — Low-Carbon Battery Materials

The Nordic region, particularly Sweden, is building low-carbon battery material supply chains to support Europe’s growing EV industry.

Access to clean energy and strong environmental standards make the region attractive for sustainable graphite production.

Key characteristics

Clean electricity for energy-intensive processing

Strong ESG and regulatory frameworks

Close proximity to European gigafactories

Key project

Talga Group — Integrated graphite-to-anode production in Sweden

The region’s role will likely focus on regional supply for European battery manufacturers.

4. Japan and South Korea — Advanced Battery Material Expertise

Japan and South Korea play a critical role in the graphite supply chain through advanced materials engineering and anode manufacturing.

While these countries have limited graphite resources, they are leaders in battery material processing and technology.

Key characteristics

Mature battery supply chains

Strong materials science capabilities

Close integration with global automakers

Major companies

POSCO Future M (South Korea)

JFE Chemical (Japan)

Mitsubishi Chemical (Japan)

These manufacturers typically specialize in high-performance anode materials and synthetic graphite production.

How Should You Diversify Graphite Anode Sourcing Now?

The graphite supply chain is still evolving. New mines are opening, processing capacity is expanding, and battery demand is growing quickly. For sourcing teams, the goal is simple: reduce concentration risk while securing long-term supply.

Below are practical strategies to diversify graphite anode sourcing.

1. Build a Multi-Region Supply Strategy

Avoid relying on a single country or supplier. A resilient graphite supply chain typically spans multiple regions, each specializing in a different stage.

For example:

Africa — natural graphite mining

North America / Europe — graphite processing and anode material production

Japan / South Korea — advanced battery material manufacturing

This structure reduces exposure to export controls, tariffs, and geopolitical risks.

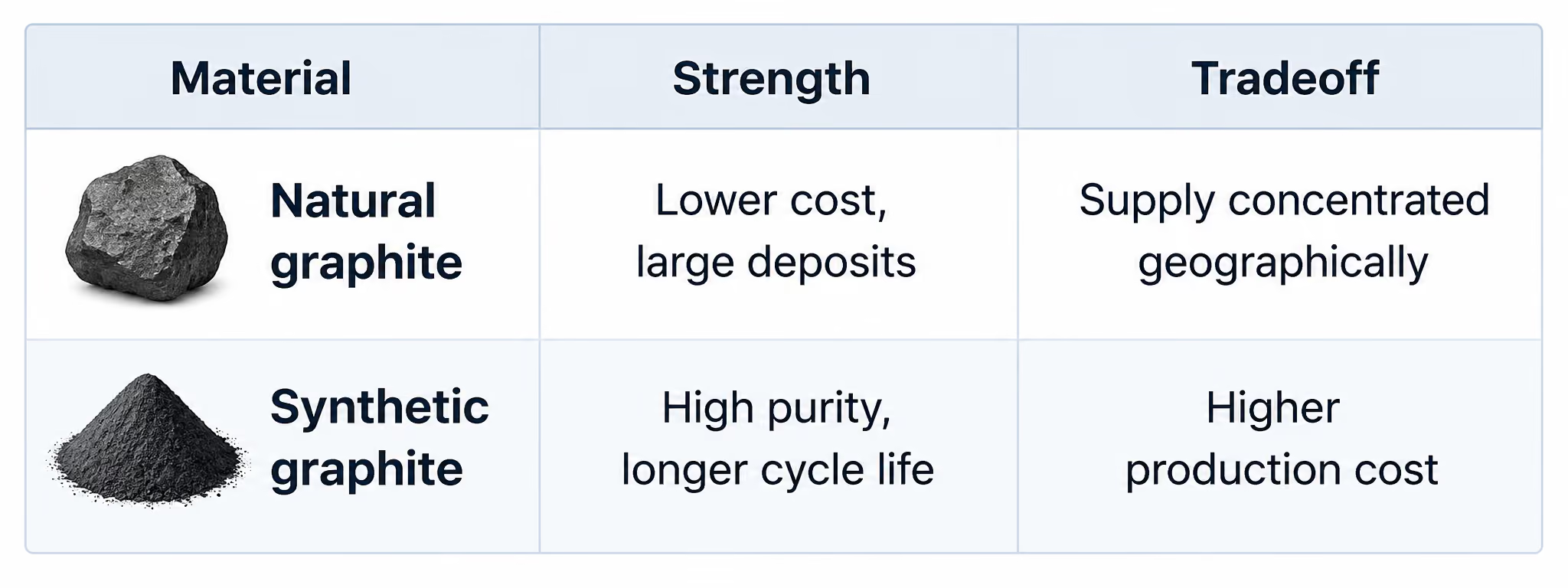

2. Combine Natural and Synthetic Graphite

Most EV batteries already use a blend of natural and synthetic graphite.

Each material serves a different purpose:

Using both materials gives sourcing teams flexibility and redundancy.

3. Secure Long-Term Offtake Agreements

Graphite projects require significant capital investment. To finance expansion, suppliers typically need long-term purchase commitments.

Common contract structures include:

5–10 year supply agreements

Indexed pricing linked to graphite markets

Volume commitments tied to battery production

Locking in supply early helps avoid shortages as EV demand accelerates.

4. Use Data Tools to Identify Verified Suppliers

Finding reliable graphite suppliers is difficult because the industry is fragmented and opaque. Many projects are early-stage, and supplier information can be incomplete.

Tools like SourceReady, an AI supplier search engine, help sourcing teams quickly identify and verify potential suppliers by analyzing trade data, certifications, and manufacturing capabilities.

With structured supplier data, you can:

Discover non-China graphite producers and processors

Verify supplier credentials and production capabilities

Compare suppliers across regions and materials

This makes it easier to build a diversified and resilient sourcing strategy.

Conclusion

Graphite supply for EV batteries is entering a transition period. While China will remain a major supplier, governments and battery manufacturers are actively building alternative supply chains across multiple regions. New capacity from companies like Syrah Resources, Novonix, POSCO Future M, Talga Group, and Nouveau Monde Graphite shows that diversification is already underway.

For sourcing teams, the priority is resilience. That means diversifying across regions, combining natural and synthetic graphite, and securing long-term supply agreements. Tools like SourceReady can also help identify verified suppliers and emerging producers faster. As EV demand grows through the late 2020s, companies that secure diversified graphite sourcing today will be far better positioned tomorrow.

FAQ

1. Why does China dominate the graphite anode supply chain?

China controls most of the processing capacity, not just the mining.

China’s advantages include:

Established spherical graphite processing

Large-scale anode manufacturing

Lower production costs

Deep expertise in battery material engineering

2. What are the main types of graphite used in EV batteries?

Two types are commonly used:

Natural graphite

Mined from graphite deposits

Lower cost

Requires purification and processing

Synthetic graphite

Produced from petroleum coke

Higher purity and consistency

More expensive but offers better performance in some batteries

Most EV batteries use a blend of both materials.

Find the sourcing tools you need.

Explore how SourceReady helps you research products, discover suppliers, verify factory information, analyze trade data, and manage your sourcing workflow in one place

Graduating from USC with a background in business and marketing, Judy Chen has spent over a decade working in e-commerce, specializing in sourcing and supplier management. Her experience includes developing strategies to optimize supplier relationships and streamline procurement processes for growing businesses. As SourceReady’s blog writer, Judy leverages her deep understanding of sourcing challenges to create insightful content that helps readers navigate the complexities of global supply chains.