The Red Sea disruption exposed a structural weakness in global sourcing rather than a temporary logistics shock. From late 2023 through 2025, security risks around the Suez Canal forced major carriers to reroute Asia–Europe traffic via the Cape of Good Hope, adding 10–15 days to transit times, increasing fuel and insurance costs, and degrading schedule reliability. Because routing decisions were driven by carrier discretion and insurance pricing—not clear mandates—sourcing teams faced rolling uncertainty instead of a stable alternative. By 2025, this instability became normalized. The most exposed “suppliers” were ocean carriers, whose routing and surcharge decisions directly reshaped landed costs, working capital, and compliance risk across apparel and electronics supply chains.

Red Sea Crisis: How Shipping Disruptions Impact Costs

What actually happened in the Red Sea, and why did it matter to your supply chain?

If you strip away the headlines, the Red Sea disruption was a risk concentration failure colliding with geopolitics.

What triggered the disruption?

Starting in late 2023 and carrying through 2024 into 2025, commercial vessels transiting the Red Sea and Bab el-Mandeb Strait faced repeated security threats linked to regional conflict. These risks sat directly on the Suez Canal corridor, which normally handles ~12% of global trade and a far higher share of Asia–Europe container traffic.

The result was not a full shutdown—but something operationally worse:

- Unpredictable security risk, not a binary “open/closed” status

- Insurance repricing, not outright bans

- Carrier discretion, not government mandates

That combination forced shipping lines—not cargo owners—to decide when and whether to transit.

How did carriers respond?

By early 2024, most major container lines made the same call:

- Suspend or sharply reduce Suez transits

- Reroute Asia–Europe services via the Cape of Good Hope

- Layer on disruption, war-risk, or contingency surcharges

- Continuously reassess and reverse decisions as conditions changed

This is the key point for sourcing teams: There was no “new normal.” There was rolling uncertainty.

Some carriers briefly announced returns to the Red Sea, only to reverse course weeks later. From a planning perspective, that’s worse than a stable detour—you couldn’t lock lead times, ETAs, or cost assumptions with confidence.

Some carriers briefly announced returns to the Red Sea, only to reverse course weeks later. From a planning perspective, that’s worse than a stable detour—you couldn’t lock lead times, ETAs, or cost assumptions with confidence.

Why did this hit sourcing teams harder than expected?

Because Suez risk is asymmetric.

If you source primarily from Asia and sell into Europe, the Red Sea is not just “a route”—it’s the route that makes your lead times, MOQs, and cost models work.

Once carriers detoured around Africa:

- Transit times extended by ~10–14 days on typical Asia–Europe lanes

- Fuel consumption jumped, driving operating cost increases

- Equipment cycles slowed, tightening container availability

- Schedule reliability degraded, even when sailings weren’t cancelled

From a procurement lens, this cascaded into:

- Higher landed cost volatility

- Increased inventory-in-transit (working capital drag)

- More frequent expedites and exceptions

- Greater contract and surcharge disputes

None of that shows up neatly in a single P&L line item—but all of it shows up in audits.

Why does 2025 still matter if the crisis started earlier?

Because by 2025, the disruption had shifted from shock to structural risk.

Carriers and insurers no longer treated Red Sea risk as temporary. Instead:

- Surcharges became normalized

- Networks were redesigned with Cape routing as a baseline option

- “Return to Suez” became conditional and reversible

For sourcing leaders, that means you’re no longer managing a crisis—you’re managing persistent route instability.

And that’s exactly why the most exposed “suppliers” in 2025 weren’t just factories or OEMs. They were the shipping providers and logistics nodes sitting underneath your entire supplier network.

What did rerouting actually add in time, cost, and friction?

The Cape detour is not subtle. It’s “same goods, different physics.”

What changes when Asia–Europe avoids Suez?

- Longer transit: commonly cited +10–14 days Asia→Europe.

- Higher operating cost: more fuel burn + more vessel days + more insurance risk pricing.

- Capacity absorption: longer voyages tie up ships and boxes, tightening effective supply. DHL explicitly called out equipment impacts from prolonged transit cycles.

- Surcharges: carriers layered on disruption/contingency fees (example: Maersk kept multiple disruption-related surcharges in effect).

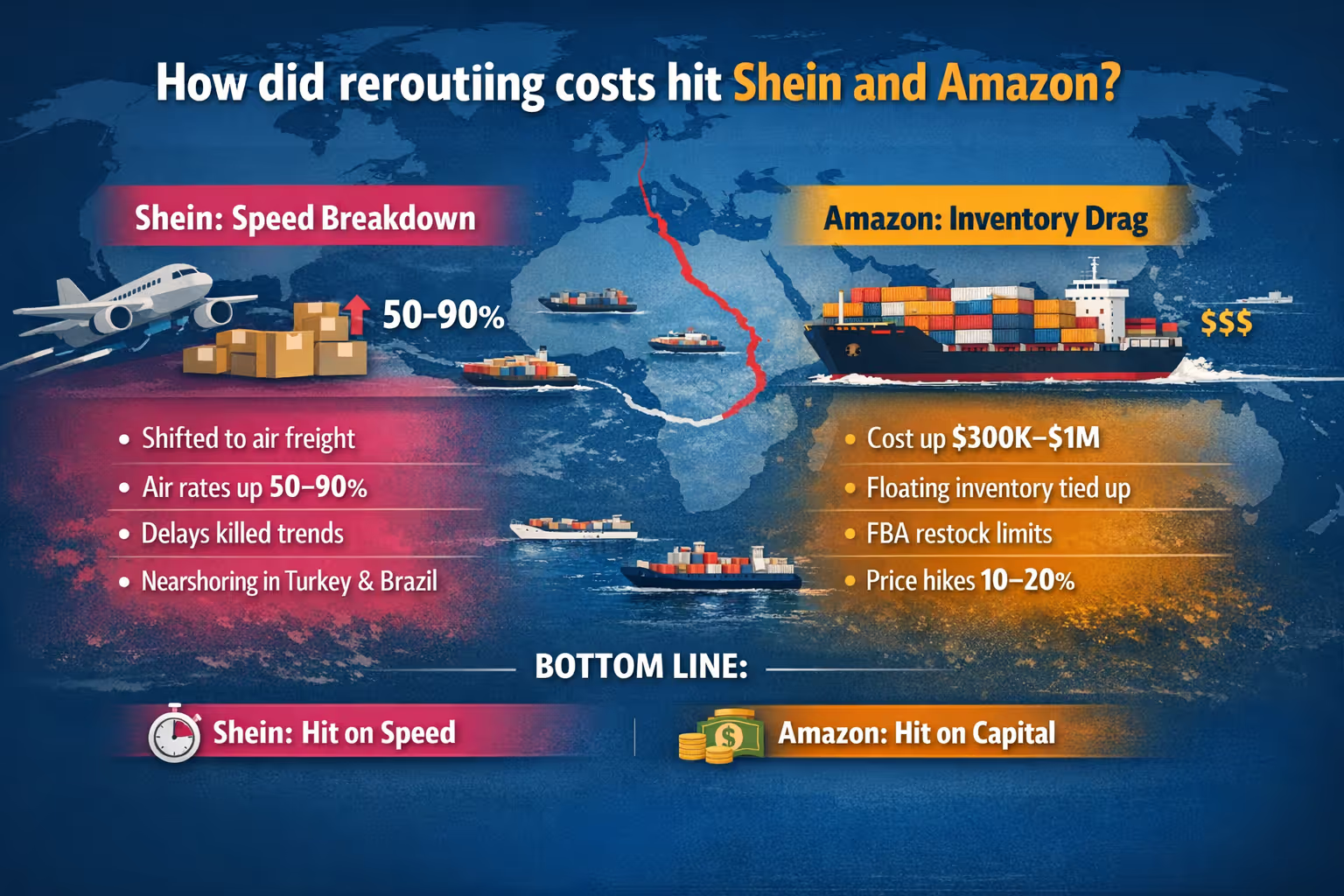

How did rerouting costs hit Shein and Amazon in the real world?

In 2025, the Red Sea crisis shifted from a temporary disruption to a "new normal" that fundamentally changed the cost structures for Shein and Amazon. While both companies were hit by longer transit times (adding 10–15 days) and higher fuel costs, their specific business models caused them to suffer in very different ways.

1. Shein: The "Air Freight" Trap

Shein’s business model is built on speed—specifically, getting a $15 dress from a factory in Guangzhou to a customer in London or New York in under 10 days.

The Pivot to Air: Because ocean shipping via the Cape of Good Hope became too slow for "ultra-fast" fashion, Shein was forced to move a massive portion of its inventory to air freight.

Cost Surge: By mid-2025, air freight rates from China to Europe spiked by nearly 50% to 90% as more companies competed for limited plane space. This effectively erased the "low-cost" advantage of Shein’s manufacturing.

The Strategic Hit: For Shein, rerouting isn't just about money; it’s about latency. If a trend lasts only three weeks, a 15-day shipping delay means the product is "dead on arrival." To combat this, Shein began rerouting its entire supply chain by opening "near-shoring" hubs in Turkey and Brazil to serve the EMEA and Americas markets without crossing the Red Sea.

2. Amazon: The "Inventory Holding" Tax

Amazon relies more on ocean freight for its bulk "Sold by Amazon" goods and the millions of tons of inventory held for third-party sellers.

Tied-Up Capital: Rerouting around Africa added roughly $300,000 to $1,000,000 in fuel and labor costs per round-trip for large container vessels. More importantly, it meant Amazon's capital was tied up in "floating inventory" for two extra weeks.

Restock Limits: In April 2025, Amazon quietly reinstated FBA restock limits, capping how much inventory sellers could send. This was a direct result of the "unreliable sea" causing bottlenecks at ports like Rotterdam and New York.

Passing the Buck: To cover these rerouting costs, Amazon increased its "Holiday Peak Surcharges" and allowed sellers to raise prices by 10–20% without losing the "Buy Box" (their fair-pricing algorithm usually punishes such hikes, but they relaxed it to prevent seller bankruptcy).

Conclusion

The Red Sea disruption didn’t break global trade—but it permanently changed how reliable your assumptions can be.

By 2025, the lesson was clear: logistics is no longer a neutral utility. Ocean carriers function as critical suppliers, and their routing and pricing decisions directly shape your landed costs, inventory exposure, and audit risk. When a single corridor underpins your sourcing model, instability doesn’t need to be catastrophic to be expensive.

The companies hit hardest were not those without scale, but those whose speed, cost, or service models quietly depended on Suez working “most of the time.” Once that assumption failed, costs surfaced in different places—air freight, excess inventory, price increases, or tighter seller controls—but they surfaced nonetheless.

For sourcing leaders, the response is not crisis management. It’s structural discipline. You need to know which suppliers and lanes are route-sensitive, which freight costs are variable, and which exceptions are truly justified. That means treating logistics exposure as part of supplier risk, not an afterthought.

Tools like SourceReady matter here because visibility is now a control mechanism. In a world of persistent routing instability, the advantage doesn’t go to the fastest responder—it goes to the team that already knows where the risk sits.

FAQ

1. Why is the Red Sea so important to global trade?

The Red Sea connects the Indian Ocean to the Mediterranean via the Suez Canal. Roughly 12% of global trade passes through this corridor, including a large share of Asia–Europe container traffic. If this route becomes unstable, vessels must detour around the Cape of Good Hope—adding time, cost, and capacity strain.

2. Did companies like Shein and Amazon switch entirely to air freight?

Not entirely—but air freight usage increased for time-sensitive goods. Air preserved speed but significantly increased costs. Larger companies also explored near-shoring, inventory pre-positioning, and routing diversification to offset delays.

3. Is the Red Sea disruption over in 2025?

Not definitively. While some carriers resumed limited transits, routing decisions remain conditional and reversible. The key issue is persistent uncertainty, not total closure.